Wealth of Possibilities

Download app

1 Million+

Active Customers

5000 Crores+

Assets Under Management

20 Million+

Transactions

Everything you need for building wealth

PMS

Elevate your financial journey with Fisdom’s expert-managed Portfolio Management Services.

Learn moreStocks and F&O

Take advantage of our powerful, user-friendly platform to invest or trade in stocks

Learn moreOwn your financial future with our all-powerful app

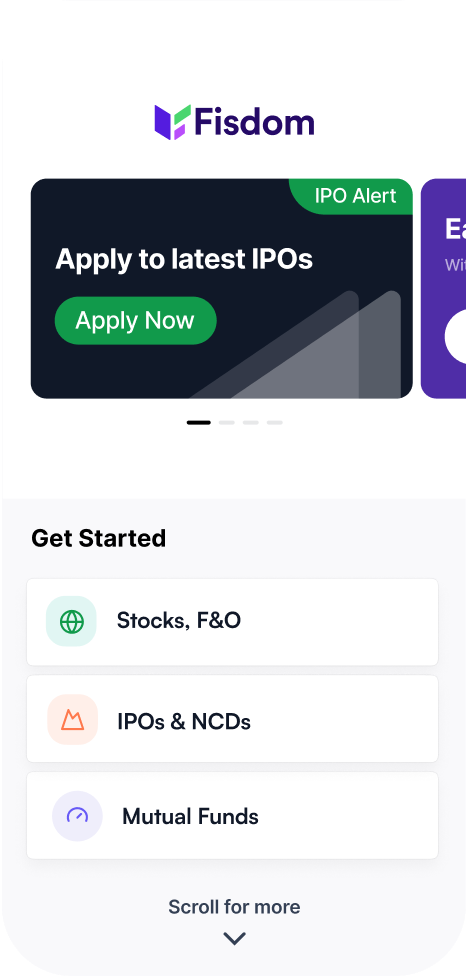

One app, multiple products

An all-inclusive suite for investing, trading, retirement planning & tax filing

Dynamic & feature-rich

Pause/Restart SIP, smart withdraw, 15+ screeners, 3500+ expert-rated stocks, Equity SIP, Margin trading facility & more

In-built intelligence at every step

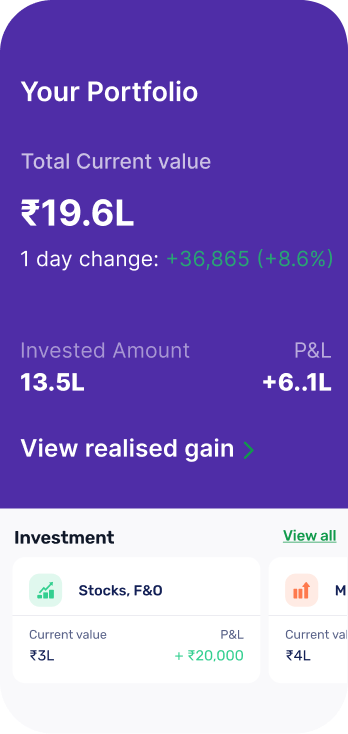

Detailed portfolio analysis & insights to keep track of your investments

How it works

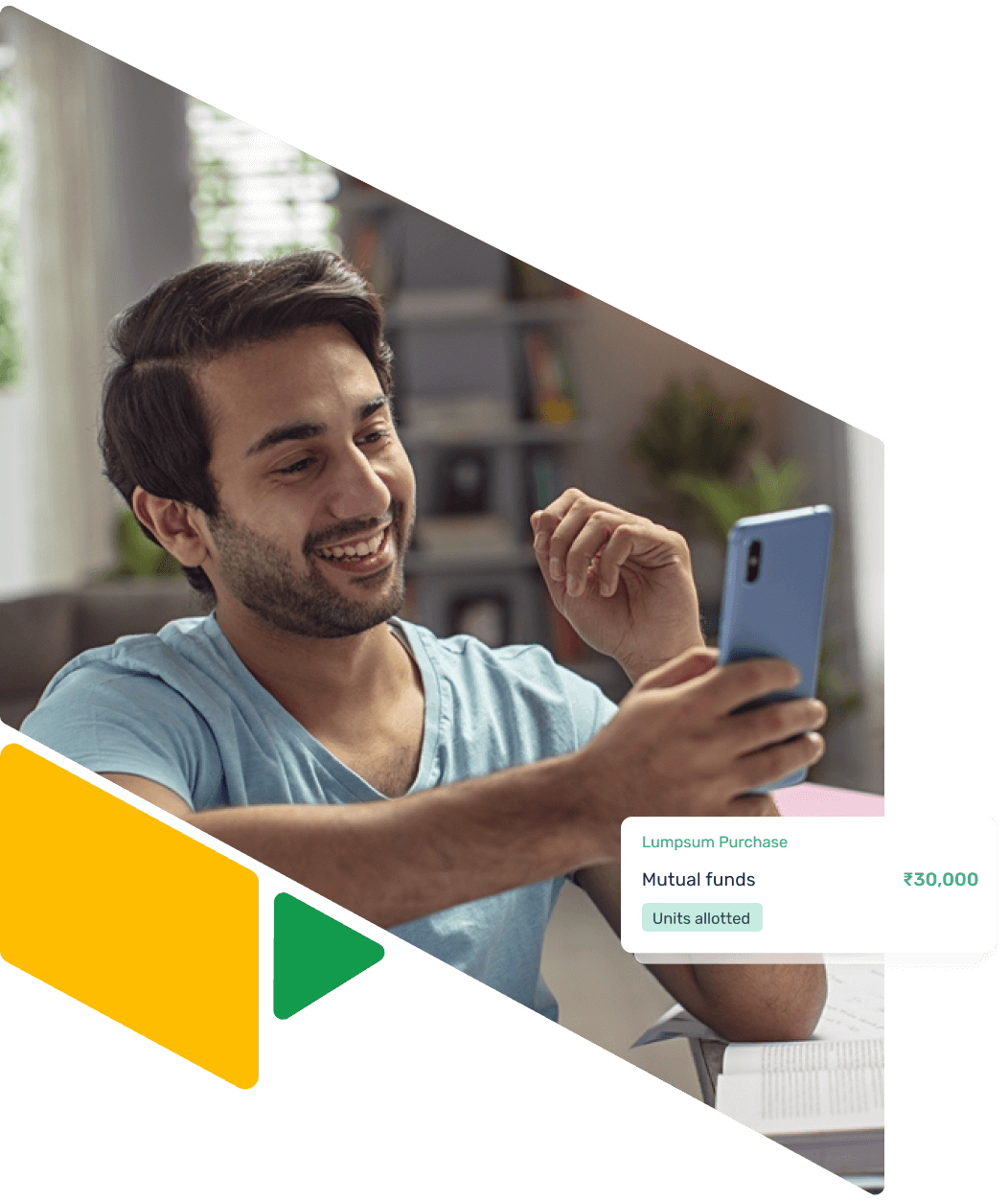

Do It Yourself

With the Fisdom app, you can trade, invest, and evaluate your portfolio with ease anytime and from anywhere With our comprehensive mobile app.

Download app

Personal Wealth Manager

Designed to cater to the needs of high networth individuals, businesses and families, Fisdom Private Wealth provides the advantage of deep research and comprehensive technology along with the luxury of a personal wealth manager.

Learn more

India's top banks trust Fisdom with their customers' wealth

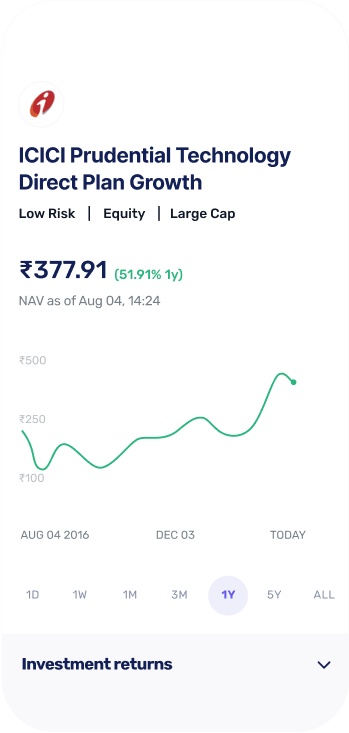

Strong research to power the investor in you

Access premium research articles, fundamental analysis on stocks, analyst reports, commentary, and accurate and indepth market insights

Learn more

Learn better, invest smarter

Youtube

Keep up with the markets

Subscribe to our YouTube channel to stay in the know. Watch live videos, fireside chats, weekly Q&As & more

Visit our channel

Blog

Investment blogs on Fisdom

Read articles on personal finance, trading, mutual funds, alternative investments, market, economy and more created by the Fisdom content team.

Start Reading

FE Best Banks Award

Fisdom received “Best Fintech Award” consecutively for 2020 & 2021

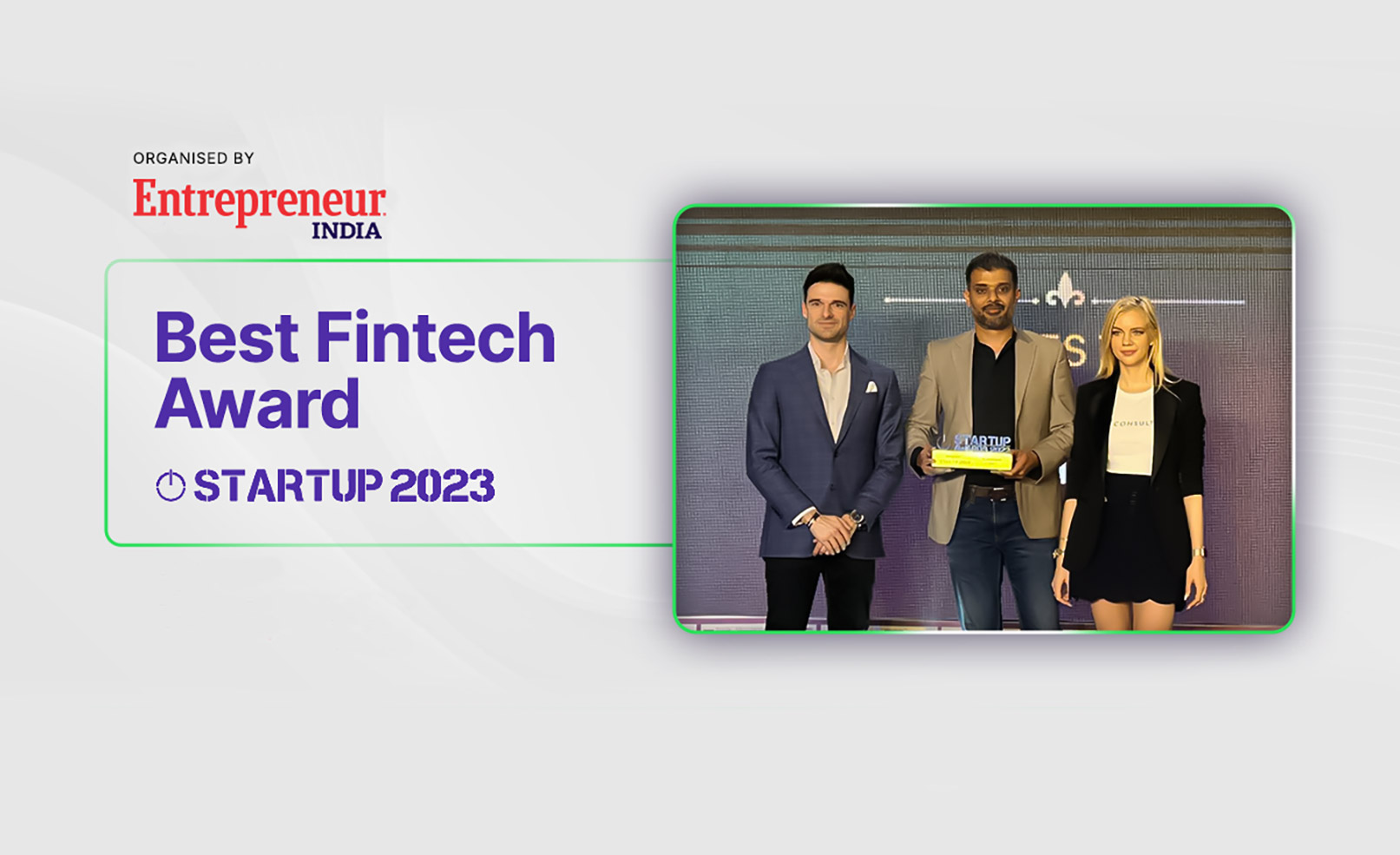

STARTUP 2023

Fisdom awarded "Best Fintech Company" at STARTUP 2023 Awards by Entrepreneur India

Bharat Fintech Awards 2023

Fisdom was awarded “Best Wealthtech” for 2022-23

BSE

BSE recognised Fisdom as “Top Fintech” for the year 2021-22

PICUP Fintech 2022

Fisdom was awarded “FICCI Best Financial Services Partner Award” in 2022

WealthTech 100

WealthTech 100 recognised Fisdom as the “Top Global WealthTech” for the years 2020 & 2021

People ❤️ Fisdom

Featured in

Download one of India's best wealth management apps

Join more than one million investors and take control of your wealth

Download app