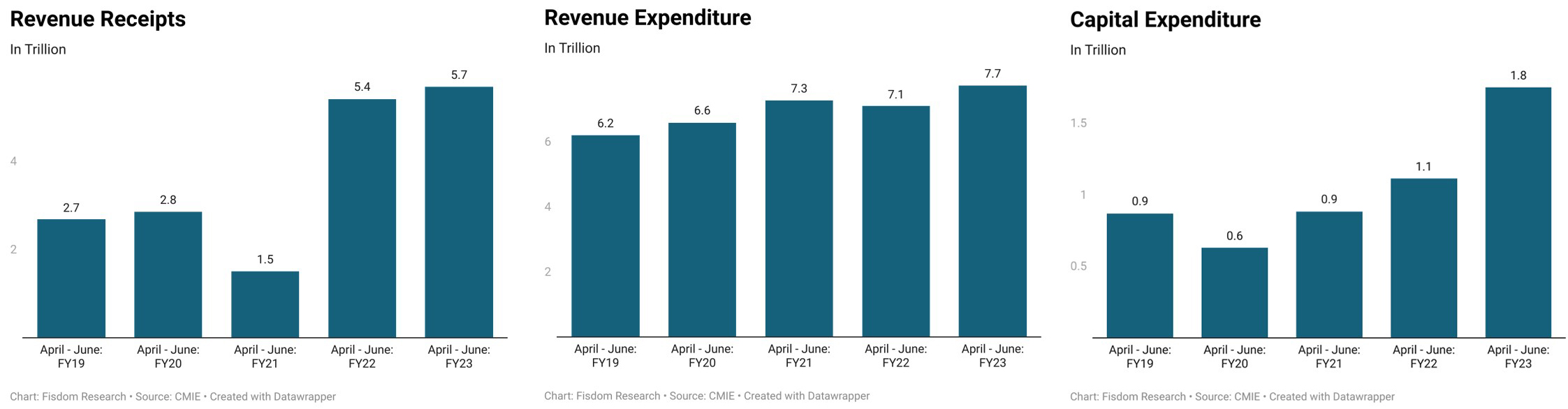

The Central Government’s first quarter performance shows that it is well on the path to spending the entire budgeted expenditure for 2022-23 without deviating from its fiscal target. The government spent Rs.9.5 trillion, or 24 per cent of its annual budgeted expenditure from April-June 2022, which is 15.4 percent higher than the expenditure incurred during the previous period a year ago.

Out of the Rs.7.5 trillion capital expenditure budget for FY23, the government has spent Rs.1.8 trillion from April-June 2022, an increase of 57 percent compared to the same period a year ago, which is much needed to spur growth. Even on the revenue expenditure front, the government has used a fourth of its budgeted revenue expenditure in Q1FY23. It was majorly driven by interest payments and then by subsidies.

When it comes to revenue, the receipts saw a remarkable growth on the back of the highest ever tax revenue collected in Q1FY23. It has mobilised Rs. 5.1 trillion in the same quarter. It was majorly driven by a 40.7 per cent jump in income taxes, a 30 percent surge in corporation taxes & 24.8 percent increase in goods & services tax (GST). The government is in a position to absorb this additional subsidy burden owing to the buoyancy in its tax collections. It does not need to compromise on its major budgeted expenditures – revenue or capital. Hence we don’t expect any dent in the government’s budgeted numbers.

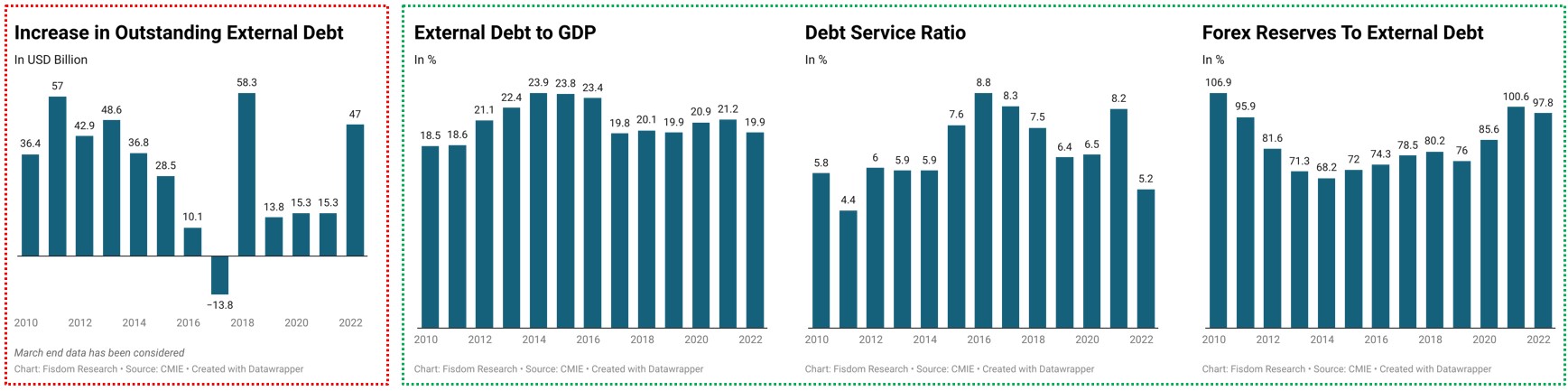

India’s external debt situation seems reasonably placed; short-term debt still a concern

Of the total outstanding external debt, 43.1 per cent will mature in the next year. Almost 96-98 per cent of short-term debt by original maturity is trade-related credit raised by non-financial corporations. The 20 per cent increase in outstanding trade-related credit is due to the steep rise in India’s imports during 2021-22, led by the sharp increase in global commodity prices, including energy and food prices.

The debt service ratio of interest payments and principal repayments to current receipts – dropped to an 11-year low of 5.2 per cent by end-March 2022. It is because of a sharp increase in current receipts to USD 798.7 billion during FY22.

The ratio of foreign exchange reserves to total debt was 97.8 per cent by end-March 2022. A quicker increase in outstanding external debt compared to forex reserves is the critical reason for a lower ratio. The ratio will likely deteriorate further, given the drop in foreign exchange reserves.

Most indicators determining external debt sustainability appear to align with the past trend. However, there are troubles regarding short-term debt; given the pressure, it can exert on the sharply depreciated rupee.

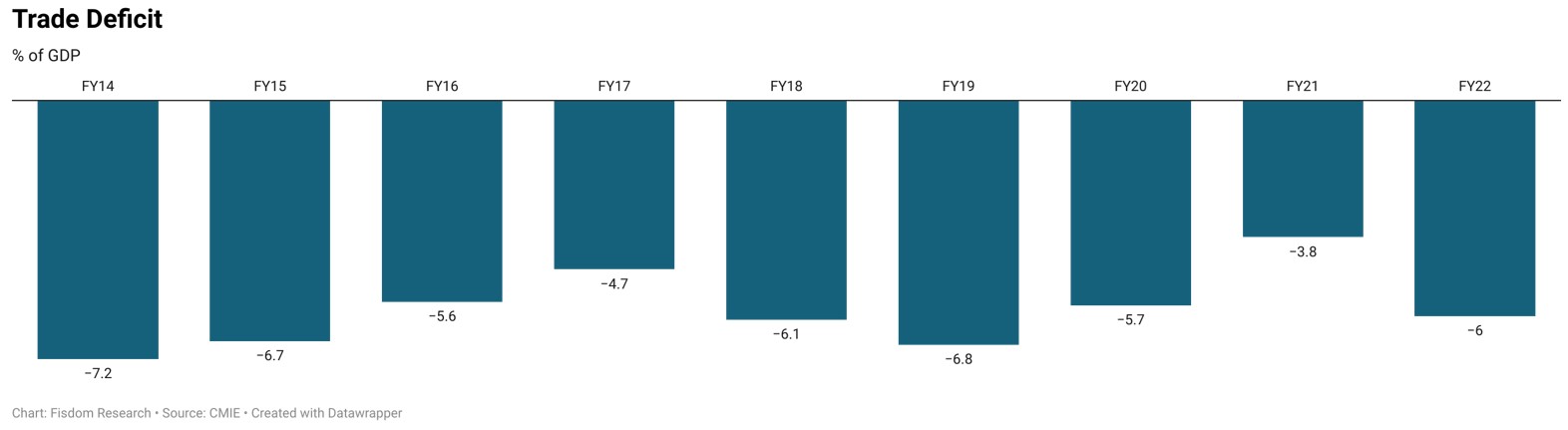

Trade deficit continues to expand

India’s merchandise trade deficit rose rapidly and peaked at USD 70.8 billion during the quarter that ended June 2022. Half the deficit during the quarter was derived from trade in POL, and the other half from non-POL items. Imports rose at a faster clip than exports.

The record high trade deficit has two macroeconomic implications for the Indian economy. Firstly, it results in the widening of the current account deficit (CAD), which along with the foreign portfolio investments (FPI) flight, is currently exerting pressure on the Indian rupee. The rupee depreciation increases the landed cost of imports, thereby adding to the domestic price inflation, which is presently ruling well above the RBI’s upper limit of tolerance of 6 per cent. Secondly, the merchandise trade deficit in 2022-23 is expected to amount to 7.9 per cent of GDP, thereby eating into the economy’s growth. It will be the highest pie of GDP eaten away by merchandise trade deficit in the last ten years.

We expect India’s merchandise trade deficit to remain elevated in the next two quarters – those ending in September and December 2022. The deficit will likely ease in the March 2023 quarter following the decline of imports due to an expected easing of global commodity prices.

Download the full report to get the complete coverage