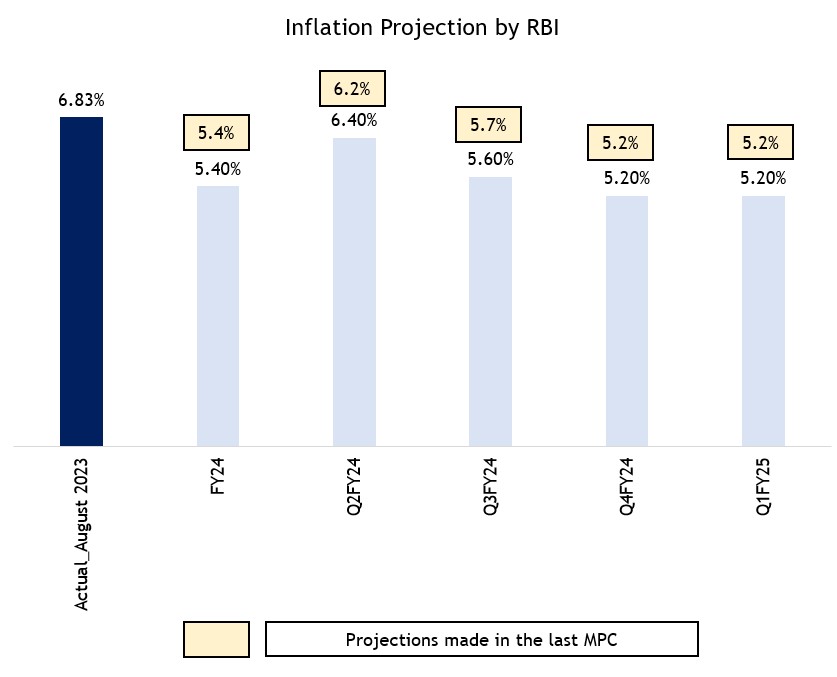

Headline inflation surged in July-August due to food prices but is expected to ease. Core inflation is moderating.

Growth

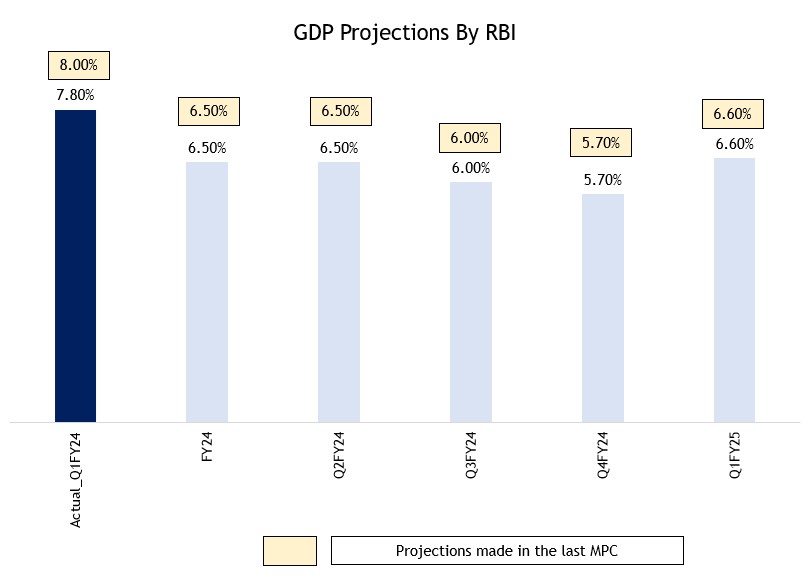

Domestic economic activity is resilient, with strong domestic demand. Investment activity is robust.

Liquidity

Efforts to manage excess liquidity include ending the incremental cash reserve ratio (I-CRR) and possible OMO-sales.

Financial Stability

Indian banking system is resilient with improved asset quality.

External Sector

Exports and imports have been contracting, but services exports are strong. Foreign exchange reserves are rising.

Additional Measures

Various measures introduced, including changes to prudential norms, extension of payment infrastructure development fund scheme, and more.

Bottomline

Commitment to align inflation with the 4% target while supporting growth and maintaining financial stability.

Near-term inflation uptick signals, but long-term projections remain stable.

Aspect

Inflation Outlook

Near-Term Outlook

Expected improvement due to vegetable price correction and reduced LPG prices.

Future Trajectory Factors

Lower area sown under pulses, dip in reservoir levels, El Niño conditions, and global energy and food price volatility.

Manufacturing Firms

Expect higher input cost pressures and marginally lower growth in selling prices in Q3 compared to the previous quarter.

Services and Infrastructure Firms

Expect a moderation in the growth of input costs and selling prices.

Source: RBI, Fisdom Research

Q1FY24 GDP falls short of projections, future growth outlook remains unchanged

Aspect

Growth Outlook

Factors Supporting Domestic Demand

Sustained buoyancy in services

Rural demand revival

Optimism in consumer and business sentiment

The government’s focus on capital expenditure

Healthy financial conditions for banks and corporates.

Global Headwinds

Geopolitical tensions

Volatile financial markets

Energy price fluctuations

Climate-related shocks pose potential risks to growth.

Source: RBI, Fisdom Research

RBI’s tight liquidity signal spurs long-end yield surge

RBI’s primary concern is the excessive liquidity in the banking system and its potential impact on price and financial stability.

The introduction of the Incremental Cash Reserve Ratio (I-CRR) and its subsequent phase-out demonstrates RBI’s commitment to effective liquidity management.

RBI emphasizes the need for banks to proactively manage their liquidity, as seen in its encouragement for participation in 14-day variable rate reverse repo (VRRR) operations over parking funds in the SDF.

RBI’s readiness to consider Open Market Operation sales (OMO-sales) reflects its flexibility in using tools to align liquidity conditions with its monetary policy stance, aiming for a balanced and stable environment. OMO sales, to achieve this balance.

As a result of these measures, the impact on long-term yields has been more pronounced than on short-term yields.

India

Before MPC

After MPC

Change (In Bps)

10 Year G-sec

7.21%

7.36%

+15 bps

7 Year G-sec

7.25%

7.40%

+15 bps

5 Year G-sec

7.24%

7.42%

+18 bps

3 Year G-sec

7.26%

7.38%

+12 bps

Source: RBI, Fisdom Research

Download the full report to get the complete coverage