What’s happening in the debt market now?

Long Term yield: India’s 10-year g-sec yield hardened by 32bps YTD21 as on 25th February 2021 and 12bps post budget FY22(01st February till date as on 25th February 2021). This comes after an earlier softening of 59bps from 01st March 2020 till the end of CY20.

Short term yield: India’s 3-year g-sec yield hardened by 65bps YTD21 as on 25th February 2021 and 22bps post budget FY22 till 25th February 2021. Yields had softened by 135bps from 01st March 2020 till the end of CY20.

Reasons for recent YTD hardening in the yield curve:

– The Government announced a borrowing target of INR.12.05 lakh crore for FY22 while increasing the borrowing target for FY21 by INR.80,000 crore to 12.8 lakh crore. The Government targeting a fiscal deficit of 4.5% of GDP by FY 2025-26 through fairly steady decline over the period. Fiscal deficit in BE 2021-2022 is estimated to be 6.8% of GDP.

Impact: Government securities need to be sold to meet the borrowing target for the current and next financial year. This will lead to more supply of government securities in the market. The supply will eventually result in bond prices moving down and consequently the yield harden. The roadmap of consolidation of the deficit is perceived bumpy by bond street.

– Reserve Bank of India has revised the inflation target to 5% in H1 FY22 and 4.3% in Q3 FY22, with risk broadly balanced. Core inflation remains elevated at 5.5%. Expectation of increase in commodity prices may add further upside pressure to the inflation.

Impact: RBI has maintained an accommodative stance for a while now, which may be difficult to sustain if inflation continues to rise. The governments intend to raise money from the market to make up the growth subdued because of Covid. Upside risks to inflation can be expected to tag along with growth.

With no attached scope for further easing, We do expect a major uptick demand for long term gsecs in the near term.

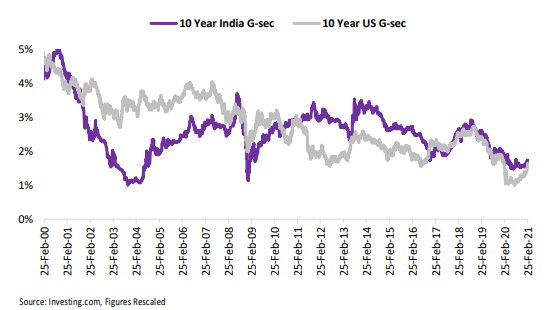

– US 10-year g-sec yield have gone up from 0.9% to 1.53% while inflation has risen to 2%. It is on track to exceed 2% for some time. Adding to this, the new US government is planning to announce a $1.9 trillion aid package.

Impact: Though the US Fed intends to maintain lower rates for longer, the US g-sec participants have reacted to news on the stimulus & transitionary inflation. We are yet to observe meaningful intent or directions on actions to cap yields. Till further clarity emerges, the yield can be expected to harden in the near term. India 10-year g-sec and US 10-year g-sec have been observed to exhibit a moderately strong positive correlation.

This further supports the case for hardening in India 10-year g-sec in the very near term. In such a case, we can expect foreign investors to sell off some Indian bond holdings as its premia becomes rich.

1.0: Correlation – India’s 10-year g-sec vs US 10-year g-sec

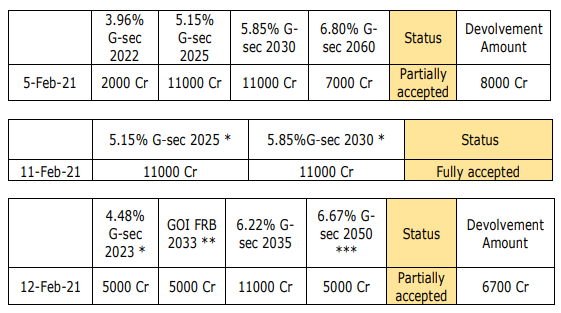

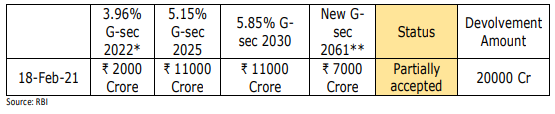

– Bond street worry of bumping at lower yield; central banker refuses to offer more.

Starting 05th February 2021 till 18th February 2021, the central bank ran four distinct auctions for long dated securities. Only one out four was executed successfully. While rest all rounds witnessed partial or very low subscription. Below mentioned are the list of auctions done in February 2021:

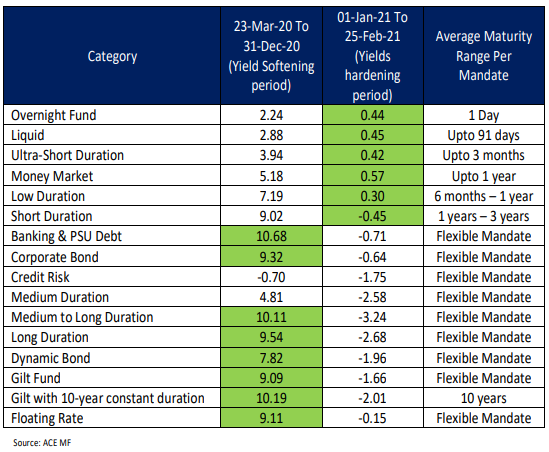

Debt Mutual Fund Analysis: Category Level Performance (Absolute/Category Average)

Longer maturity funds did well during the easing cycle and shorter durations performed relatively better during the hardening. However, the performance of categories can not be attributed only to the duration exposure but also to a variety of attributes including aggregate yield on underlying strategy and implementation of strategy. However, duration is the key contextual metric defining portfolio quality and expected performance.

In line with our aforementioned interpretation of the situation, we have observed fund categories with a flexible mandate and previously stretched duration are trimming exposures, albeit gradually with a bias towards accrual strategy in most cases.

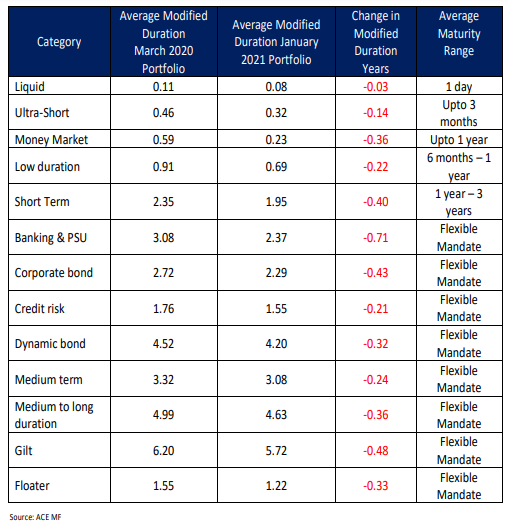

Duration Change (In Years): Category Level

Observations:

– 90% of the categories had trimmed the portfolio exposure to ~3 years. We have seen this trend across categories.

– Also, the funds have the flexible mandate to change the duration as and when needed.

Key Takeaways:

For Existing Investors:

Existing investors who have invested with a sound strategy and robust asset allocation need not react to the news flow and market dynamics as fund managers continue to optimize per evolving dynamics.

New investors:

New investors must approach debt investing basis a sound financial plan and robust asset allocation strategy. While fund managers continue to optimize funds, investors must refrain from taking aggressive duration calls and steer clear from taking exposure to securities rated below sovereign and AAA/A1 and equivalent.