What Is The Latest Reading?

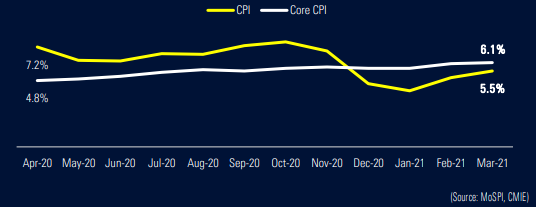

India’s inflationary trend has welcomed 1st quarter of CY21 with an upwards-scaling trend, increasing for the second consecutive month. Recording 5.52% (4-month high) in Mar’2021, inflation figures registered 5.03% and 4.06% (16-month low) in Feb and in Jan’21, inching near the upper limit of RBI’s tolerance level of 6%. Core CPI followed suit of increasing trend, registering 6.1% vs 6.0% in the month prior

The inflation-targeting framework of of 4(+/-2)% band is to be adopted for the next five years up to March 2026, ending speculation about more vouching for liberal interest-expensive stance to boost growth. Any further loosening can undermine the central bank’s ability to set effective onetary policy.

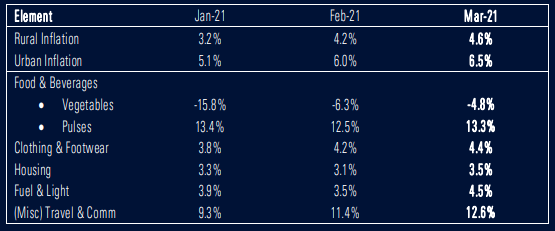

Element Inflations

Analyst Commentary

The rise in inflation can be credited to sharp upticks witnessed in food (oil, meat & non-alcoholic beverages), fuel, and transportation costs. Rising commodity prices, and pass-through pricing power courtesy of demand normalization pose as upside risks to inflation readings in near-term.

High base-effect coming into play in later part of this year can see inflation paint benign figures.

This can lead to misguiding of real inflation figures in H1CY2021.

The uptick in food basket can be attributed to price rise in oil, and pulses & products. Crude oil (WTI) prices surged on the hopes of an improvement in demand due to COVID-19 vaccinations.

Declining crude oil inventories in U.S., tighter supplies from OPEC, and rising govt. taxes, further supported oil prices to reach its pre-pandemic level, adding to inflation level.

As pressures on perishable food prices ready for a go on the downside, other factors such as supply-side disruptions, and higher labor charges can dampen hopes of drop in inflation in coming times.

The relatively higher level of core inflation reflects second round impact of persistent oil price hikes, higher import duties, rising input prices and feverish demand. Same is confirmed by visible uptrend in goods rather than services (housing, education) which continue to be benign.

In last bi-monthly monetary policy meeting, the central bank kept its key interest rates unchanged while maintaining its accommodative stance. Continuing to focus on growth via polices and packages, RBI is to use an arsenal of unique liquidity and similar supportive strategies to maintain current pace of expedited growth.

Broad-based domestic and global economic recovery should improve aggregate demand, posing an upside risk to inflation. Appreciating rupee and any risk of new covid-strain led slowdown, will be a tailwind for CPI inflation.

It is likely for RBI to remain on pause in next meet and consider rate-cuts in near future after efficacy in transmission of prior rate-cuts.

Click here to read MoSPI’s original press release on “New CPI For March, 2021”