Extended Pause, Policy Comfort Holds as Inflation Troughs

The Reserve Bank of India’s February 2026 policy marked a continuation of the extended pause, with the MPC unanimously maintaining the policy repo rate at 5.25% and retaining a neutral stance. The decision was widely expected, but the policy communication reinforced an important shift: the easing cycle is firmly behind us, and the focus has decisively moved to transmission, liquidity management, and durability of growth.

While headline inflation remains well below the tolerance band, the RBI acknowledged that the disinflationary phase is past its trough, with base effects and precious metals inflation likely to push CPI closer to the 4% target in early FY27. Growth, meanwhile, continues to surprise on the upside, supported by resilient domestic demand, services momentum, and improving investment conditions. Against this backdrop, the MPC sees little urgency to recalibrate rates, preferring to preserve policy flexibility amid global uncertainty.

TL; DR

- Repo rate unchanged at 5.25%, SDF at 5.00%, MSF/Bank Rate at 5.50%

- Neutral stance retained; one member continued to favour a shift to accommodative

- FY26 GDP growth pegged at 7.4%, with Q1 & Q2 FY27 revised up to 6.9% and 7.0%

- FY26 CPI inflation projected at 2.1%, rising to ~4.0–4.2% in early FY27 on base effects

- Liquidity remains in surplus, backed by aggressive OMOs, FX swaps and VRRs since December

- Policy emphasis squarely on transmission, liquidity smoothing, and financial stability

Investment View: With the rate-cut cycle clearly behind us and inflation moving off its trough, the scope for incremental duration-led capital gains is limited. The February policy reinforces the RBI’s preference for holding rates steady for an extended period while ensuring orderly liquidity and effective transmission of past easing.

In this environment, accrual rather than duration is likely to be the dominant return driver. Elevated spreads in high-quality credit, temporary tightness in money markets due to seasonal factors, and a stable policy rate outlook create a favourable setup for short-to-medium maturity strategies.

Growth: Domestic Momentum Offsets Global Noise

The RBI revised FY26 real GDP growth to 7.4%, supported by robust private consumption, resilient rural demand, and steady investment activity. Services continue to outperform, manufacturing has shown signs of revival, and government capex remains a key anchor for growth

| Period | Dec-25 | Feb-26 |

| FY26 | 7.3% | 7.4%⬆️ |

| Q1FY27 | 6.7% | 6.9%⬆️ |

| Q2FY27 | 6.8% | 7.0%⬆️ |

For FY27, near-term momentum remains strong, with Q1 and Q2 growth revised upwards. Trade deals with the EU and progress on the US agreement offer incremental support to exports, even as geopolitical tensions and global financial volatility persist.

Our View: The growth-inflation trade-off currently tilts in favour of growth support without compromising stability. However, with growth holding up better than expected, the bar for further monetary easing is high. Policy support is now more likely to come through liquidity operations and regulatory measures rather than rate action.

Inflation: Trough Behind Us, Normalisation Ahead

Headline CPI inflation remained exceptionally low in November–December 2025 (0.7% and 1.3%), driven by sustained food deflation and benign fuel prices. Core inflation has remained range-bound, excluding the sharp rise in precious metals prices, which alone contributed ~60–70 bps to headline inflation.

Looking ahead, the RBI expects inflation to edge higher from Q4 FY26 onwards, largely due to adverse base effects rather than demand-side pressures. CPI inflation is now projected at 3.2% in Q4 FY26, rising further to 4.0%–4.2% in Q1–Q2 FY27. Importantly, the RBI continues to emphasise that underlying inflation pressures remain muted, with food supply prospects, buffer stocks, and rabi sowing conditions providing comfort.

The marginal upward revision in the inflation path relative to the December policy confirms that headline inflation has likely bottomed out. The normalisation toward the 4% target is expected to be gradual and driven more by base effects and precious metals prices rather than any resurgence in core demand pressures.

| Period | Dec-25 | Feb-26 |

| FY26 | 2.0% | 2.1%⬆️ |

| Q1FY27 | 3.9% | 4.0%⬆️ |

| Q2FY27 | 4.0% | 4.2%⬆️ |

Our View: The February policy confirms that India is transitioning from an unusually benign inflation phase to a more normalised inflation environment closer to target. This reduces the probability of further rate cuts and shifts the policy debate from “how much easing?” to “how long the pause lasts”. Inflation risks are now more symmetric, with precious metals, energy volatility, and weather-related disruptions being key monitorables.

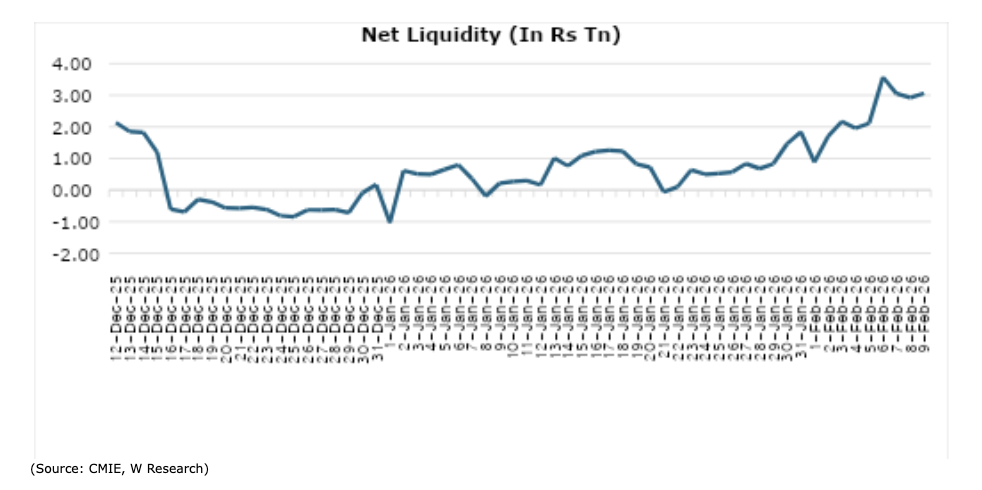

Liquidity & Transmission: Heavy Lifting Already Done

System liquidity remains comfortable, supported by substantial durable liquidity infusion undertaken since December 2025. Over the past few months, the RBI has cumulatively injected more than ₹7.5 lakh crore through a combination of open market purchases, USD/INR buy–sell swaps and longer-tenor variable rate repo operations. Even after accounting for currency leakage and CRR-related absorption, estimates suggest that core liquidity has remained in a healthy surplus through January 2026.

Transmission of the cumulative 125 bps policy rate cuts has continued to progress. Lending rates on fresh loans have declined meaningfully, while deposit rates have softened with a lag. Money market rates experienced temporary tightness in January due to seasonal factors, redemption bunching and moderation in headline surplus, but overall liquidity conditions remain adequate to support credit growth and orderly market functioning.

Importantly, the RBI has reiterated that liquidity management will remain pre-emptive and flexible, with sufficient buffers to absorb fluctuations in government balances, currency in circulation and forex operations. At the same time, the central bank has signalled a preference for allowing market yields to reflect broader global conditions and supply dynamics, while using liquidity tools primarily to facilitate transmission rather than to cap bond yields.

Our View: Liquidity conditions are unlikely to be a binding constraint over the near term. With the RBI having already delivered substantial durable liquidity support, the focus has clearly shifted to smoothing short-term liquidity frictions and improving transmission. This reinforces the case for accrual-oriented strategies, as incremental policy support is more likely to come through liquidity management rather than further rate action.

Way Forward

- The easing cycle is complete; policy rates are likely on hold for an extended period

- Inflation normalisation and resilient growth reduce urgency for further cuts

- Global developments, bond supply dynamics, and inflation prints will guide future stance shifts

- Any future policy debate is more likely around timing of eventual normalisation, not renewed easing

Investment Strategy Fixed Income: Accrual Over Duration

| Scenario | Macro Backdrop | Strategy |

| Base Case | CPI normalises toward 4%, growth resilient, RBI on hold | Accrual-focused positioning |

| Bull Case | Inflation stays below target longer | Selective duration extension |

| Risk Case | Global shocks / supply-side inflation | Reduce duration risk |

| Growth Upside | Capex + reforms sustain momentum | Blend accrual with equity |

Bottom Line

February 2026 policy reinforces that India is in a policy comfort zone—low inflation, strong growth, and ample liquidity. The RBI’s challenge is no longer stimulus delivery, but managing expectations and ensuring stability. For investors, this argues for a shift from chasing duration gains to harvesting carry and spreads, while staying nimble amid global uncertainty.

Implications for Equity Markets

The February policy is modestly supportive for equities, primarily by reducing policy uncertainty rather than by adding incremental stimulus. With inflation normalising gradually and the RBI clearly signalling an extended pause, the interest rate outlook has become more predictable, improving visibility for earnings and valuation assumptions.

Comfortable systemic liquidity and the RBI’s commitment to proactive liquidity management should help maintain supportive financial conditions, even as global bond yields and risk sentiment remain volatile. Importantly, the absence of further rate cuts is offset by resilient domestic growth and improving investment momentum, which continue to underpin earnings prospects.

Our View: The policy backdrop favours an earnings-led equity market rather than a liquidity-driven rerating phase. While global factors may drive short-term volatility, the domestic macro environment remains supportive, with returns likely to be driven by earnings delivery and stock selection rather than broad multiple expansion.

Standard Disclaimer