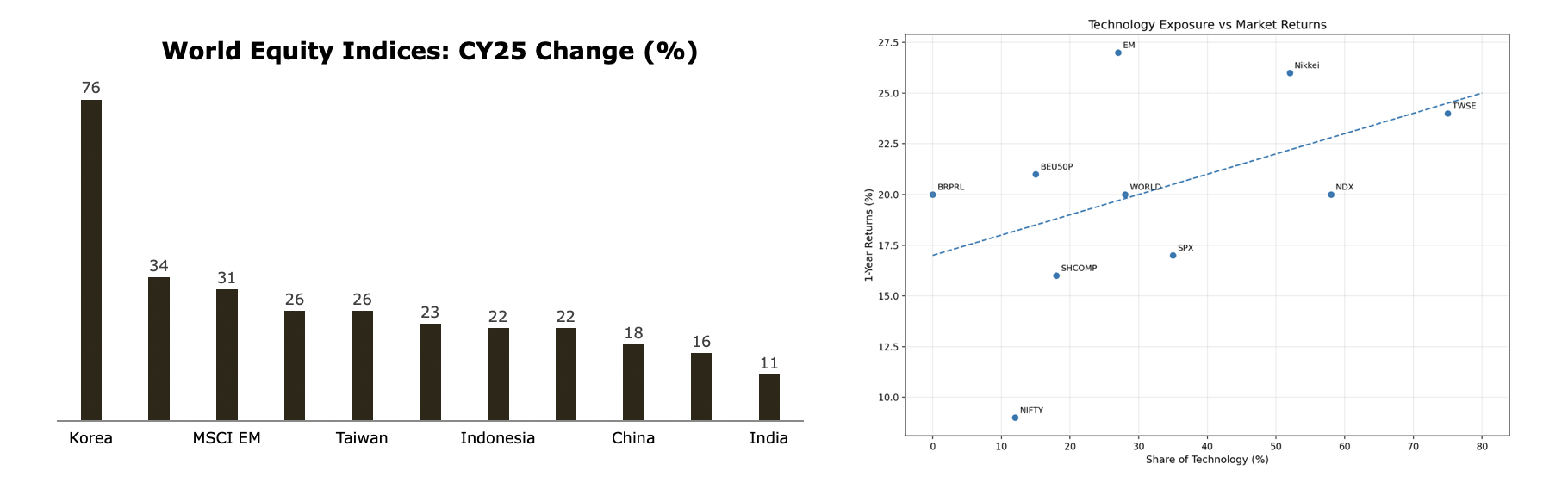

India’s 2025 Underperformance: Cyclical, Not Structural

FPI outflows driven by valuations, weak earnings and low exposure to the global AI trade

- India underperformed global markets in CY25 amid heavy FPI outflows (~USD18.9bn) and limited participation in the global AI-driven rally.

- Elevated valuations and slower earnings growth reduced India’s relative appeal versus tech-heavy markets such as Korea, Taiwan, and the US. As global capital concentrated in AI-linked sectors, India’s near-zero exposure became a drag on returns. However, valuations in India have cooled over the last year, especially in SMIDs, while global markets have turned more expensive. Earnings momentum is expected to improve meaningfully in FY27, supported by a favorable domestic macro cycle and stimulus-led recovery.

- As the global AI trade matures and India’s valuation premium narrows, the probability of FPI flows returning increases, though currency stability remains a near-term risk.

(Source: Bloomberg, Emkay Research, Fisdom Research)

Performance Summary – Sector-wise

2025 marks a shift toward selective sector leadership

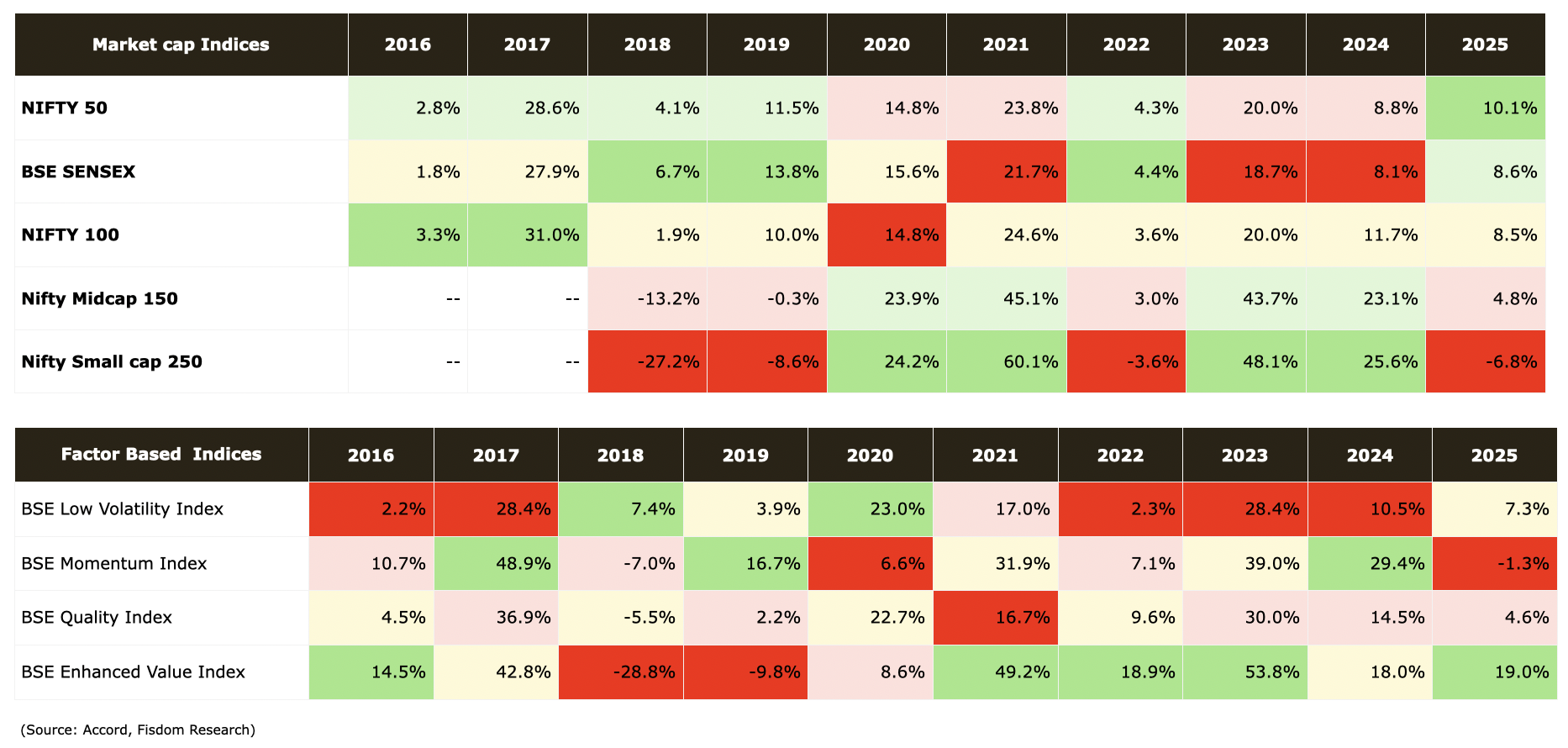

Performance Summary – Marketcap-wise & Factor-wise

2025 reflects a phase where index and factor returns are shaped by select pockets rather than broad participation

Macro Summary

Macro stability improving, but growth recovery remains uneven

What has changed

- India’s macro environment has continued to stabilise over the past month. Inflation has moderated meaningfully across headline and core measures, easing cost pressures and allowing monetary conditions to turn gradually more accommodative.

- Financial conditions have improved, with adequate liquidity and steady credit growth, although rate transmission remains incomplete. At the same time, growth indicators remain mixed — services activity is resilient, while industrial momentum and power demand have softened.

Our macro assessment

- The economy appears to be transitioning into a lower-inflation, more stable macro phase, reducing downside risks to growth. However, the recovery is not yet broad-based.

- Consumption trends remain uneven, with urban demand showing clearer signs of recovery, supported by tax relief and easing inflation, while rural conditions remain cautious amid moderating farm income growth. On the fiscal side, slower tax buoyancy has begun to constrain flexibility, even as capital expenditure remains supportive.

Way forward

- Sustainability of the macro recovery will depend on whether easier financial conditions translate into stronger private consumption and investment.

- Urban demand is likely to lead near-term growth, while rural recovery may lag until income visibility improves. External pressures — including currency weakness, trade deficits, and global uncertainty — are likely to persist but remain manageable. Overall, the macro backdrop is improving, but the next leg of growth will require stronger follow-through in demand rather than further policy support.

Key Headwinds

Weak tax buoyancy | Capex momentum slowing at the margin | INR Depreciation | Global trade and geopolitical risks | Rising Japanese Interest Rates

Key Tailwinds

Disinflation-led real income support | Front-loaded public capex cushion | Urban consumption momentum | Potential external relief triggers | Scope for easier financial conditions.