Macro Summary: Growth Stable, Drivers Rotating

Macro Tracker

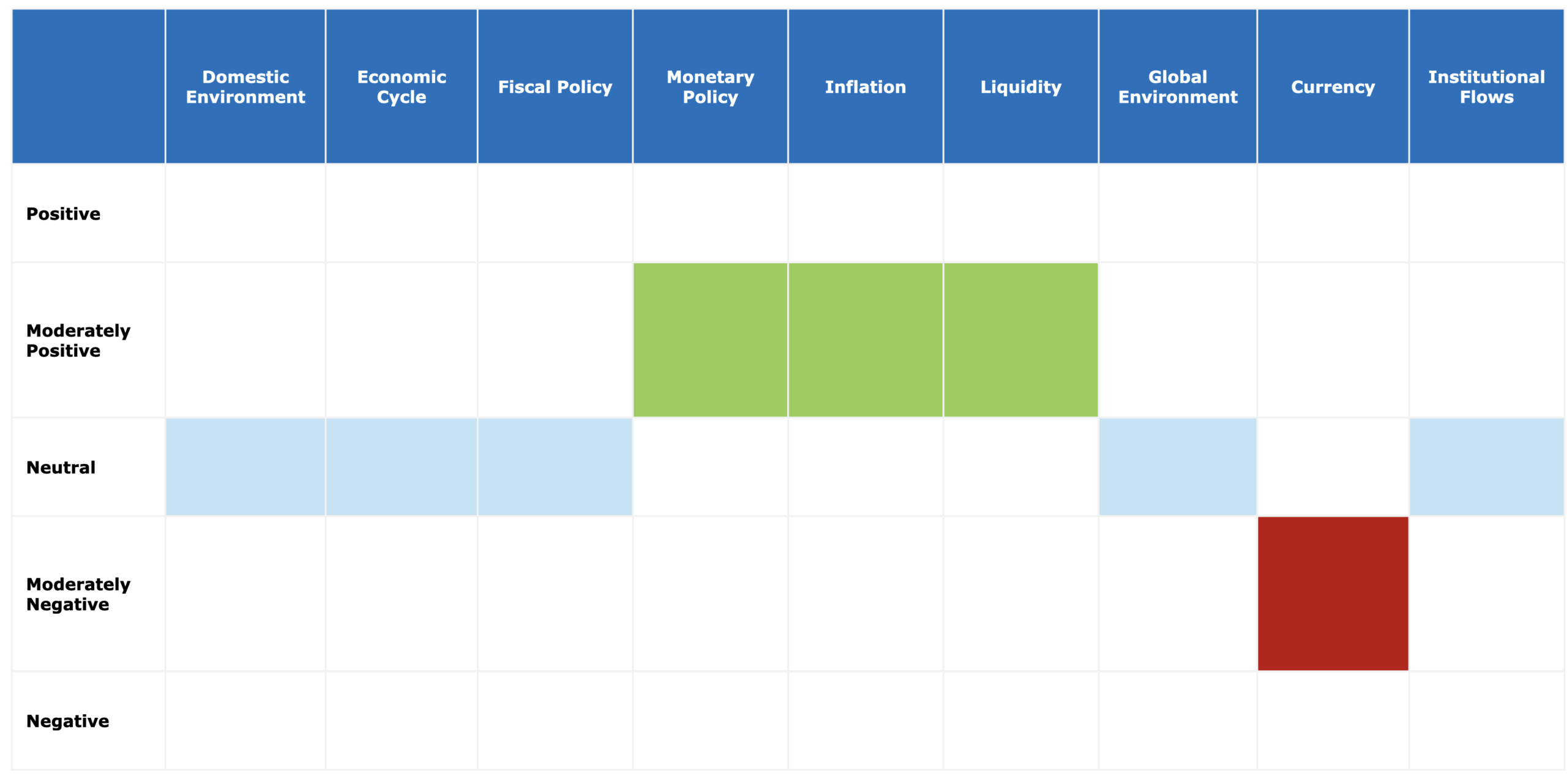

Current economic positioning

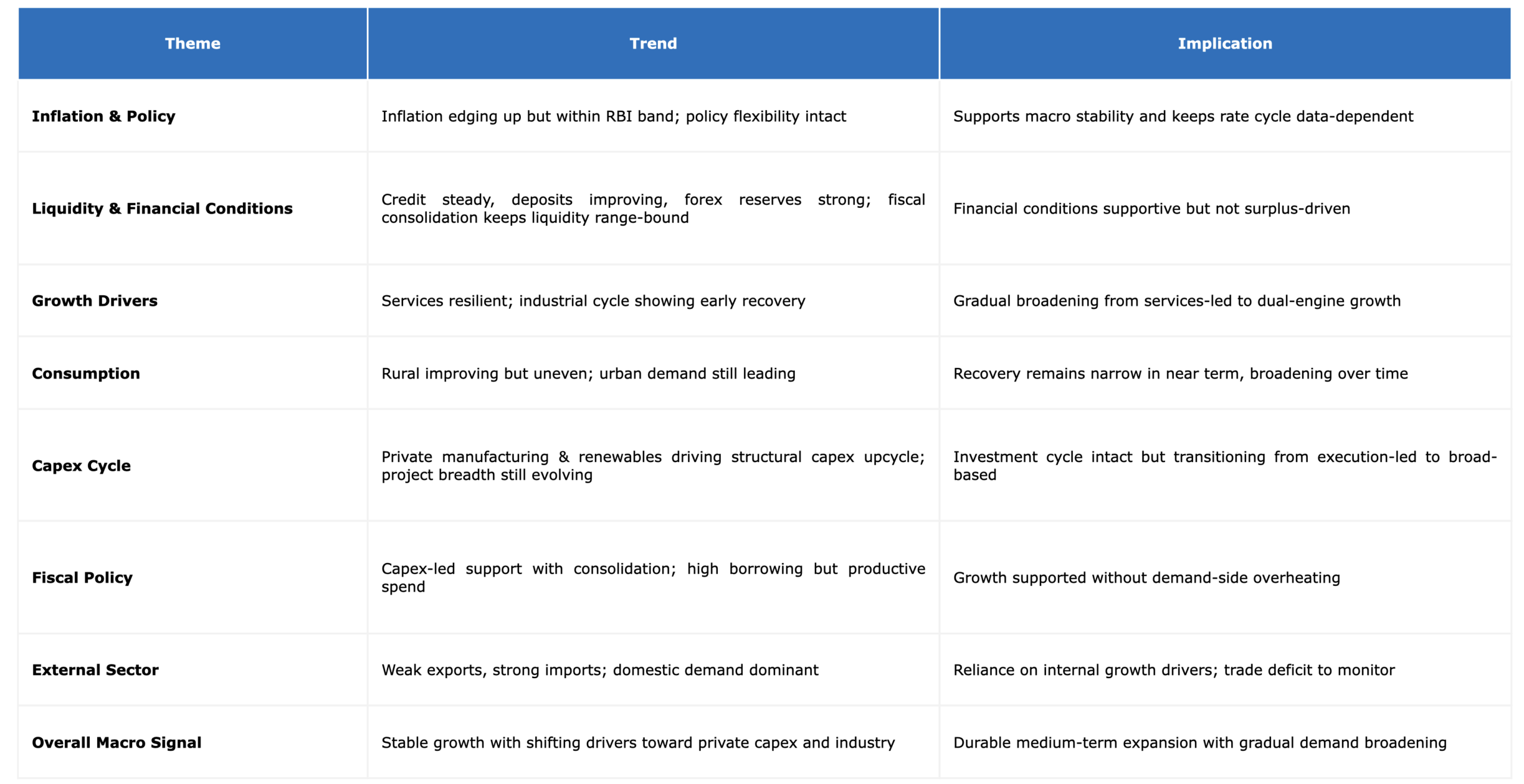

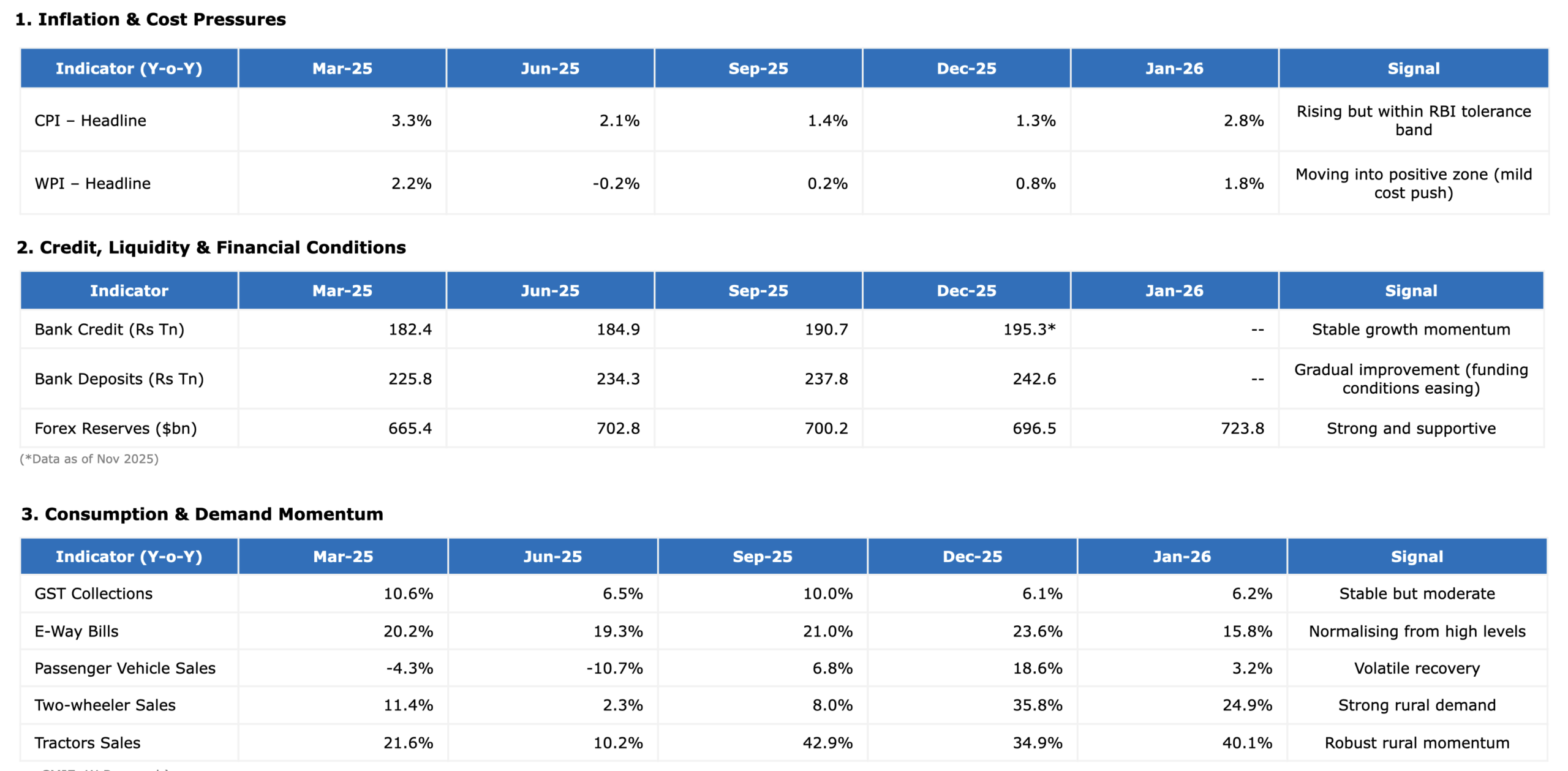

Macro Dashboard (1/2)

Domestic fundamentals stable; inflation edges up, demand mixed

(Source: CMIE, W Research)

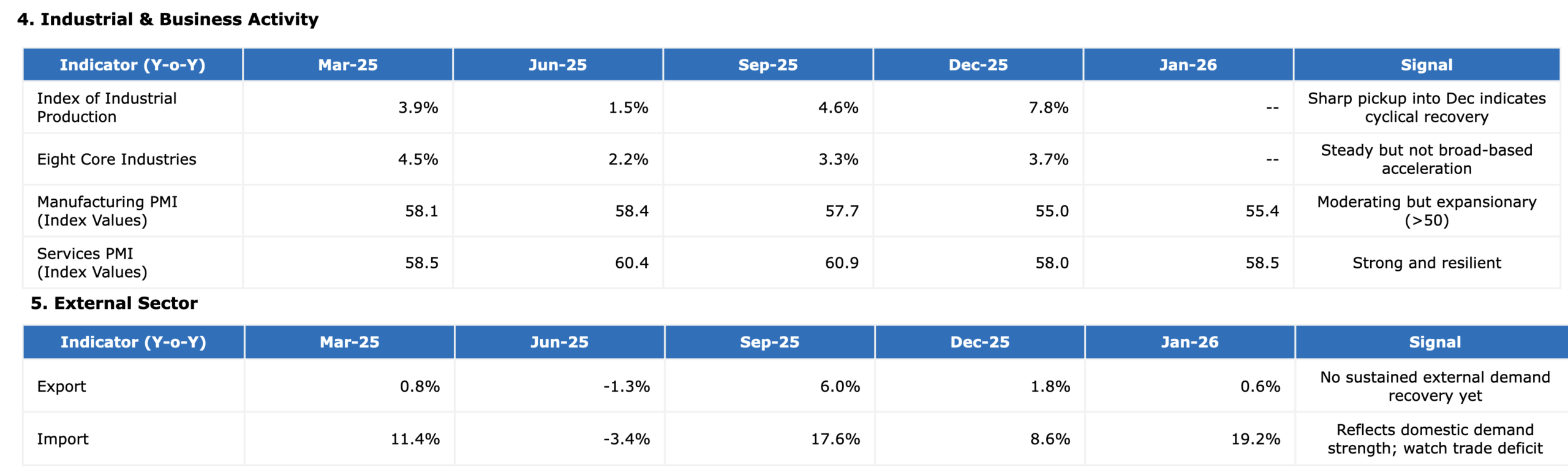

Macro Dashboard (2/2)

Industrial Recovery Emerging; External Demand Still Soft

- Over the past year, India’s macro backdrop has transitioned from disinflation to a phase of mild inflation uptick, though price pressures remain within the RBI’s tolerance band, preserving policy flexibility. Financial conditions continue to be supportive, with steady bank credit growth, improving deposit mobilization and strong forex reserves providing systemic stability.

- Growth dynamics remain domestically driven and services-led. Industrial activity has shown signs of cyclical recovery, reflected in the pickup in IIP, while PMIs remain comfortably in expansion territory despite some moderation. Consumption trends are mixed — rural demand remains robust (two-wheelers and tractors), urban discretionary is uneven (PV volatility), and GST collections point to stable but moderate demand.

- On the external front, the absence of a sustained export recovery alongside strong import growth highlights reliance on domestic demand and warrants monitoring of the trade deficit, especially amid global uncertainty.

- Looking ahead, the durability of the growth upcycle will depend on whether improving industrial momentum and supportive financial conditions translate into a broader consumption and investment recovery, while keeping an eye on the trajectory of inflation and external headwinds.

(Source: CMIE, W Research)

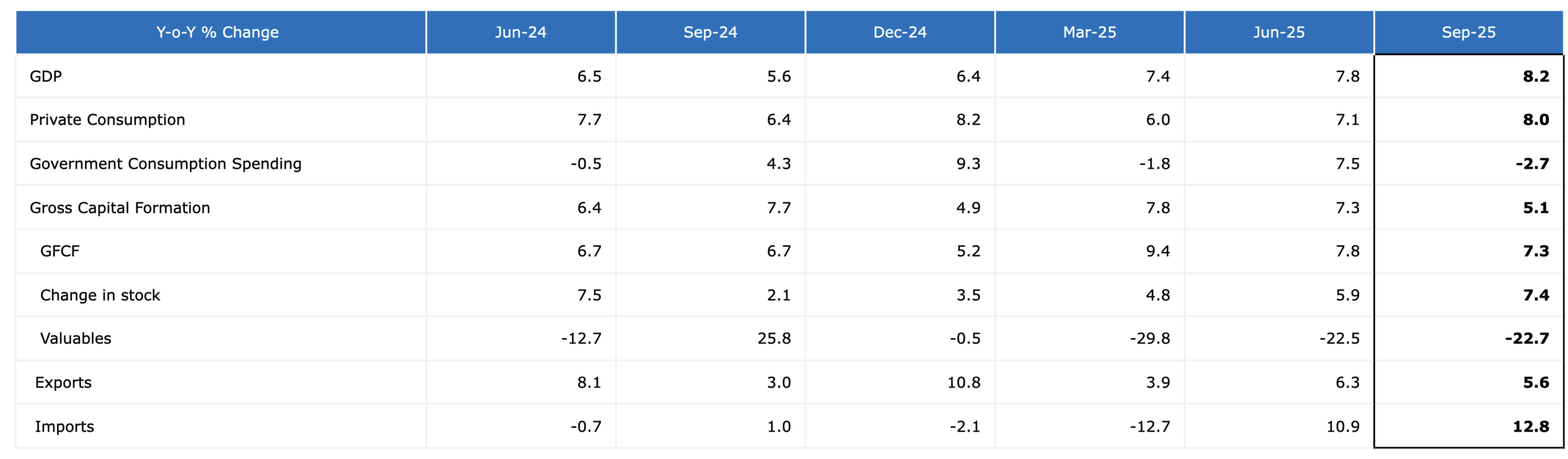

Growth Stable, Drivers Shifting

Consumption recovery gradual; capex remains the anchor

Notes:

Private Consumption: Total spending by households on goods and services | Government Consumption Spending: Government’s day-to-day spending on services like salaries, Defence and administration (not capex)| Gross Capital Formation: Total investment activity; indicates strength of the capex cycle.

- India’s GDP growth is expected to remain resilient at ~7.3–7.5% in FY26, supported by a recovery in private consumption and sustained public capex, while investment activity (GFCF) remains the second key pillar of growth. However, the moderation to ~6.5–6.8% in FY27 reflects a normalization from the post-pandemic rebound and a slower global environment.

- The data shows consumption is stabilising but not accelerating sharply, while government spending is becoming more volatile, shifting the growth impulse toward private capex and manufacturing. With exports improving modestly and imports reflecting domestic demand strength, the growth mix is transitioning from public-led to a more balanced consumption–investment cycle.

- The key monitorable for FY27 is the breadth of consumption recovery, which will determine whether growth sustains closer to 7% or trends toward the lower end of forecasts.

(Source: CMIE, W Research)