Reading the title, you must be thinking why this week’s newsletter has you reading about taxes and scrutinizing the headline as ‘click-bait’y. Especially given that many satisfied the tax man’s qualms, not less than month-&-a-half ago.

Revisit that ordeal and you will find one trait echoing the voices of the majority. This unionized calling is of the many who find themselves scrambling for plans and policies at the very last minute to shed their payables.

It is this urgency that has us talking of tomorrow’s taxes today itself. What many don’t realize is that their jab at saving pennies does more harm than good, simply because more invisible wealth is erased than visible wealth pocketed.

The key element behind successful tax planning is Time. If one does not wait for rains to come to fix their roof, then why must one wait to fix the taxes on their financials. This as simple as rarely practiced logic also happens to be the Top secret to help you not only save but also get smart with your taxes. You must have heard many say, “Early bird gets the worm”, and with this read you’ll know why.

In meriting the benefits of starting early, it is important to acknowledge tax-saving as investing and not saving expenses. The difference lies in expense being a current consumption but investments being a deferred consumption. The reason for delay is to welcome growth, a.k.a., returns. Tax saving instruments yield returns too, which if delayed can cause deep dents on your wallet width.

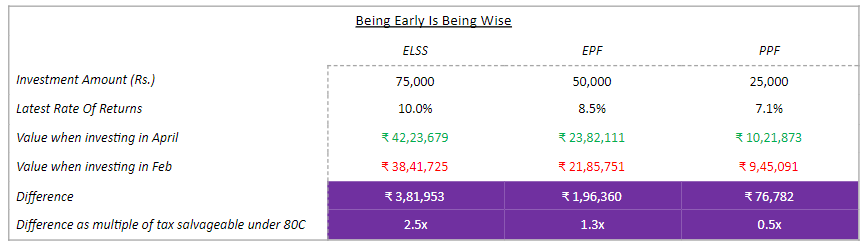

In testing the hypotheses, we made a few assumptions and calculated the math behind. The assumptions are as follows:

- Investments are made across three elements available for tax exemption under section 80C

- The return rates are assumed for ELSS category and as latest available rates for other two products

- Tax-saver undertakes SIP over 20 years on April and February of a financial year

The table below highlights the opportunity cost of delaying your tax-saving execution:

The wealth saved by early execution of tax-saving strategies evidently is a more money-favorite strategy. This approach helps you hit tow birds with one stone, as you not only save wealth but also lower your tax outgo.

Being early to the party carries a host of smaller benefits as well. A few are mentioned in brief for your reference:

- Optimal Use Of Allowances

To be nimble with taxes is to be agile with your free-use cash. For an activity regarded as mind-numbing, tax-filing is very dynamic in nature. Reckoned as every budget’s most followed announcement, quick to act tax-savers adept themselves with the new norms right from the get-go as opposed to the late bloomers who are left at the mercy of “salesmen”. Those who optimize budget process have more free green to waive around at times desired.

- Monthly Cash Management

Managing money follows hierarchy in treating expenses as primary with remainders subject to remainder-like treatment. This approach treats investing, and thus tax management, in an on-available manner. It is recommended to immediately incorporate discipline in the latter as well to ensure calibrated entry in tax0saving products and avoiding a hurried lumpsum flow on judgement day. Besides, this bodes better for return potential as well.

- Public Provident Fund (PPF)

Interest is calculated on minimum PPF balance between fifth and the end of each month. If fresh deposits are made after fifth, you miss interest for that month on that quantum. Thus, even on a shorter time-frame your laziness in tax filing can cost eat into your potential IRRs.

Apart from the aforementioned points, a key issue lies in the Range Of Choice For Tax Management. On eve’s day, all instruments appear better than the one before making for improper and impromptu paisa-pinching decisions.

In shining light on the same, lets talk of Section 80C. This section is arguably the most familiar, albeit crowded, investment + insurance tax-efficient mix of the lot. It covers a wide range of line-items such as PPF, ELSS investments, insurance premiums, home loan principal payments and children’s tuition fee among others.

The current limit of Rs 1.5 lakh is accrued by canopying various sections in 80C, 80CCC and 80CCD (1). This deductible amount was set in 2014, with it being revised just the before over the last ~2 decades. It was In 2003, that this deductible was set at Rs. 1 lakh, thus making improvements amounting to meager ~2.5% annually. This annual increase in deductions is not even at par with the inflation growth in the same period.

Given the favorability and tax-spread of this section, it is easy to exhaust the Rs.1.5 lakh amount but difficult to extract maximum value for the buck. To allocate amounts within the components requires time so as to not drain realizable value of monies when draining tax.

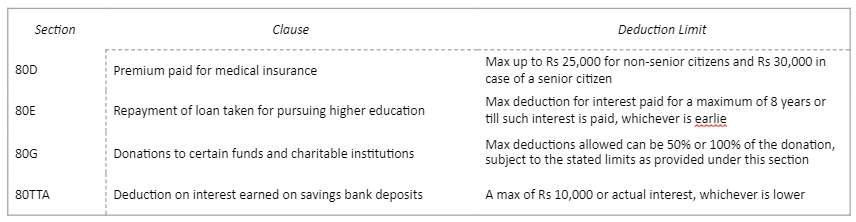

On broadening sight, tax-savers are introduced to more sections under the ITR act offering lucrative shedding opportunities. They are as follows:

On a broader level, tax planning is more than it appears to be and thus merits a proportionate amount of time. We at fisdom can cater to your tax necessities via our 100% owned subsidiary in Tax2Win. It is the only online tax filing player to have strong partnerships in the B2G2C and B2B2C segment catering to every region in India.

Remember, Noah navigated the floods cause he built the ark…..ahead of time.